How to start investing with little money

How to Start Investing with Little Money

The Importance of Just Getting Started

1) Building the habit: Starting to invest, even with small amounts, helps you develop a savings and investing habit. This financial discipline will serve you well as your income grows over time.

2) Learning the ropes: Beginning with smaller amounts allows you to learn about different investment options and strategies without risking significant capital. It’s a chance to gain experience and confidence.

3) Overcoming inertia: Often, the hardest part of any journey is taking the first step. By starting to invest now, you overcome the mental barrier that might be holding you back.

Developing Your Savings and Investing Muscle💪

1) Start Small: Begin by setting aside a small, fixed amount each month for investing. Even $20 or $50 a week can make a huge difference over time.

2) Increase Gradually: As you become more comfortable with investing, try to increase your contributions over time.

3) Stay Consistent: Regular, consistent investing is key. Set up automatic transfers to ensure you stick to your plan.

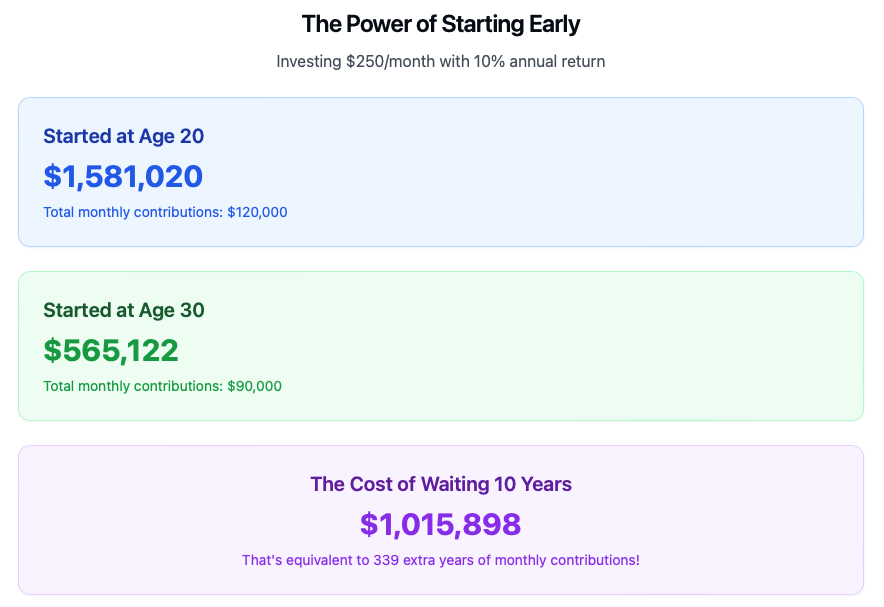

The Power of Compound Interest 📈

Here’s an example:

Want to see how your retirements can grow? 🌱

Investment Plans to Consider

When starting your investment journey, it’s important to understand the different types of accounts available. Here are some popular options:

Retirement Accounts

1) 401(k): This is an employer-sponsored retirement plan. Many employers offer matching contributions, which is essentially free money. If your employer offers a match, try to contribute at least enough to get the full match.

2) Traditional IRA: Similar to a Roth IRA, but contributions are often tax-deductible now, and you pay taxes when you withdraw the money in retirement.

3) Roth IRA: This individual retirement account allows you to contribute after-tax dollars. Your money grows tax-free, and you can withdraw it tax-free in retirement. It’s a great option for young investors or those who expect to be in a higher tax bracket in retirement.

4) SEP IRA: This is a good option for self-employed individuals or small business owners.

Taxable Investment/Savings Accounts💰

1) Taxable Brokerage Account: An account with a brokerage like Fidelity, E*Trade, Charles Schwab which allows you to invest in stocks, bonds, index funds, etc.. While you won’t have the tax benefits if a retirement account, these accounts provide more freedom and flexibility in how and when you use your money

2) High Yield Savings Account: These accounts offer a higher interest rate than a traditional savings account with the same FDIC insurance coverage. A great place to park some cash for emergencies or other short term needs

3) Certificate of Deposits (CDs): A type of savings account offered by Credit Unions or Banks which typically offer a higher interest rate than a standard savings account but do not allow for withdrawals for a specified amount of time without incurring fees.

Options to Start Investing with Little Money

1) Index Funds: These low-cost funds track a market index and offer broad market exposure.

2) Mutual Funds: While some mutual funds require higher minimal initial investments, there are plenty of options with very low initial investments to get you started on your investing journey.

3) Exchange-Traded Funds (ETFs): These offer diversification and can be purchased for the price of a single share.

4) High Yield Savings Accounts: While not technically investing, these can be a good starting point for building your financial foundation.

Understanding the Risks⚠️

The Risks of Not Investing

Resources for Beginner Investors

Books:

1) The Simple Path to Wealth by JL Collins

2) Set for Life by Scott Trench

3) The Little Book of Common Sense Investing by John C. Bogle

Websites and Online Courses:

1) Investopedia.com – A comprehensive resource for financial education

2) Khan Academy’s personal finance courses – Free in-depth lessons on investing and personal finance

3) Yahoofinance.com: For investment research, analysis, and personal finance article

Podcasts:

1) The Ramsey Show – Focuses on getting out of debt and financial discipline

2) Afford Anything – Great for understanding the psychology of money

3) Stacking Benjamins – Makes finance fun and accessible

Conclusion

What is Financial Independence, and How Do You Achieve It?

What is Financial Independence, and How Do You Achieve It?

In today’s fast-paced, consumer-driven world, more people are waking up to a life-changing goal: financial independence 💸. But what does that actually mean, and more importantly—how do you achieve it?

What is Financial Independence?

Financial independence (FI) means having enough money invested or saved that you no longer rely on active income to fund your lifestyle. In simple terms, your money works for you—whether you choose to work or not.

A common benchmark for FI is when your investments can safely cover your living expenses indefinitely. This brings us to one of the most well-known concepts in the FI community: the 4% rule.

Understanding the 4% Rule

The 4% rule is a popular guideline in the financial independence community that suggests you can withdraw 4% of your investment portfolio annually and expect it to last at least 30 years. This concept was first introduced by William Bengen, a financial advisor who published the idea in a groundbreaking article entitled Determining Withdrawal Rates Using Historical Data in 1994 . His findings were later confirmed and expanded by the Trinity Study, a research paper by three professors at Trinity University in 1998.

- If your annual expenses are $80,000, you would need $2 million invested ($80,000 ÷ 0.04).

- The rule assumes a diversified portfolio of stocks and bonds and is based on historical market performance.

🔎 Want to dive deeper?

Check out a detailed analysis by Michael Kitces in his white paper regarding safe withdrawal rates.

How to Achieve Financial Independence 🏡

Let’s break down the key habits and strategies that can accelerate your journey to financial freedom:

1. Start Early—Time Is Your Greatest Asset ⏳

Compound interest works best with time. Starting in your 20’s can mean the difference between needing $500/month versus $1,500/month in investments later on. The earlier you start, the less effort is needed to hit your goal.

📚 Want to learn more? Read this excellent primer on compound interest from Investopedia.

2. Be Consistent—Small Wins Add Up ✅

Achieving FI isn’t about winning the lottery or scoring a huge raise. It’s about consistent saving and investing, even if the amounts are modest. Automate contributions to your retirement accounts, brokerage, or high-yield savings. Over time, this discipline compounds.

👍 Check out Fidelity’s guide to dollar-cost averaging as a practical strategy.

3. Practice Financial Discipline 🔒

Discipline means saying “no” to impulse purchases, lifestyle inflation, and societal pressure to “keep up.” It also means sticking to your investment strategy even when markets are volatile. Your future self will thank you.

4. Avoid or Minimize Debt ❌

Debt is the ultimate speed bump on your FI journey. High-interest debt like credit cards can destroy your net worth faster than you can build it. Prioritize paying down debt aggressively—especially consumer debt—before ramping up investments.

🔧 Read more on the truth about debt by Dave Ramsey

5. Don’t Worry About What Others Think 🎯

The FI path often looks different from the norm. You might drive an older car, skip fancy vacations, or live below your means while others spend freely. Ignore the noise. Financial independence is freedom, and that’s far more valuable than approval.

6. Choose a Partner Who Shares Your Vision 👩🏻❤️💋👨🏻

Having a life partner who’s financially aligned with your goals is a game-changer. Shared values around saving, spending, and investing create momentum and reduce conflict. Together, you can achieve FI faster and with less stress.

The Real Benefit of Financial Independence 🌍

It’s not just about never working again. It’s about freedom:

- Freedom to walk away from toxic work environments

- Freedom to pursue passion projects

- Freedom to spend more time with family

- Freedom to live life on your terms

That’s the ultimate return on investment.

Final Thoughts 🚀

Achieving financial independence requires clarity, consistency, and courage. It’s not always easy, but it’s always worth it. Start today, stay disciplined, ignore the distractions, and partner with those who support your goals. Your future freedom depends on the choices you make now.

For more on the FI movement, check out ChooseFI’s beginner guide to reaching financial independence.

Building a Budget That Works

Building a Budget That Works For You

Building a budget that works for You: Your Path to financial success

Here’s the truth about budgeting: it only works when it works for you. The best budget isn’t about restricting everything you enjoy—it’s about balancing your goals with the life you want to live right now

💰Step 1: Determine Your Net Income

Calculate your monthly income after taxes. This would include income from side hustles, tip income, and any other income if you have it.

If you are self employed, don’t forget to account for taxes you’ll owe on this type of income. TaxAct has a self employment tax calculator which will help estimate your tax obligations.

📊 Step 2: Know Your Spending Habits

Before you begin building a budget that works for you, you will need to know where your money is going. This means tracking your expenses, no matter how small.

Make sure to include large expenses that may not occur every month. Things like property taxes, insurance payments, vacations, Christmas, etc. Estimate the annual cost of and set aside a monthly amount for these type of expenses so you’re ready when the payments are due.

Use one of these methods:

📱 Budgeting apps like Monarch Money, EveryDollar, Quicken are relatively easy to use and can connect with your accounts to simplify the process

📑 Spreadsheets can be effective if you’re organized and diligent with your receipts

📓 Notebook for those old school folks who prefer pen and paper

Pick whatever tracking method feels easiest—an app, a spreadsheet, even pen and paper. The important part is taking action, just start. You’ll probably be shocked by what you’re actually spending,

🤝 Step 3: Get on the Same Page with Your Partner

Money fights are one of the top relationship killers, but they don’t have to be. If you’re in a relationship, you need to talk money. It sounds obvious, but many couples avoid it until it becomes a problem. Getting aligned on goals and spending now saves so much drama later.

Action item: Schedule a “money date” with your partner to discuss your financial goals, concerns, and habits. Make it a regular occurrence, perhaps monthly. Be sure to discuss both necessary expenses and discretionary spending.

🎯 Step 4: Tailor Your Budget to Your Lifestyle and Goals

There’s no one-size-fits-all approach to budgeting. Your budget should reflect your lifestyle and financial goals, which is unique to you. Are you saving for a house? Planning for an early retirement? Paying off debt? Your budget should support these objectives while also allowing for some flexibility.

Action item: Write down your short-term and long-term financial goals. Then, allocate your income accordingly in your budget, making sure to include categories for both necessities and discretionary spending.

💡 Pro Budget Tip

Focus on paying off credit card, car loans, personal loans, and any other consumer debt as quickly as possible. You’ll be amazed how quickly your net worth will increase when you eliminate your debt service payements

🎉 Step 5: Set Yourself Up for Success.

A good budget isn’t just about restriction—it’s about empowerment. Include some fun funds in your budget to avoid feeling overly constrained. Also, automate your savings and bill payments where possible to make sticking to your budget easier, and avoid late fees.

Action item: Set up automatic transfers to your savings account on payday. Start small if needed—even $20 a week adds up over time.

💡 Smart Budget Strategies

Automate Your Finances

* Set up automatic bill pay

* Create automatic transfers to savings

* Use direct deposit to separate accounts

🔍 Step 6: Regularly Review and Adjust

As your life circumstances change, so should your budget. Regular review ensures that your budget continues to align with your goals and needs.

Action item: Schedule quarterly budget reviews. Assess whether your current allocations are working. Are you meeting your saving goals? Is your budget sustainable? Adjust as necessary.

🏋️♂️ Step 7: Bounce Back When You Fall Off Track

Nobody’s perfect, and there will likely be times when you overspend or forget to track an expense. The key is not to let these slip-ups derail your entire budget. Instead, view them as learning opportunities.

Action item: When you go over budget, don’t beat yourself up. Instead, analyze what happened. Was it a one-time expense or a sign that your budget needs adjusting?

If you’re having trouble staying on track, try switching to cash for items like groceries, clothing, dining out, and miscellaneous shopping.

✉️ Step 8: Try the Envelope System

This old-school method is surprisingly effective: start with some envelopes and label each one with a spending category, groceries, gas, eating out, whatever fits your life. When payday hits, fill each envelope with the cash you’ve budgeted for that category.

The rule? When an envelope’s empty, you’re done spending in that category until next payday. And before you think about “borrowing” from another envelope—don’t. That’s how the system falls apart.

Here’s why it works: There’s something about physically handing over cash that makes spending feel more real than swiping a card ever will.

Final Thoughts

Keep in mind: nobody builds a perfect budget on day one. It’s a skill you build over time, so give yourself grace when things don’t go as expected. Budgeting doesn’t have to be perfect, but you should be making progress. Stick with it, adjust as you go, and actually acknowledge when you’re doing well. Those wins matter and build momentum.

The beauty of a budget that works for you is it doesn’t feel like sacrifice. You’re not choosing between enjoying today and securing tomorrow, creating a budget that works for you will help you do both. After all, the point of getting your finances together isn’t just to watch numbers grow in a savings account. It’s about building a life where money supports your dreams instead of holding you back.

Poor is a State of Mind

Poor is a State of Mind

Poor Is a State of Mind: 5 Steps to Build a Growth-Oriented Money Mindset

I know the phrase “poor is a state of mind” can raise eyebrows. To be clear: this isn’t about dismissing real financial struggles, ignoring economic barriers, or blaming individuals for their current circumstances. `Instead, it’s about recognizing one powerful truth—your financial mindset can either trap you in limitation or propel you toward resilience, creativity, and growth.

How a Positive Money Mindset Can Transform Your Finances ✨

Life will always throw challenges your way—but your money mindset and how you respond determines the outcome. A strong, growth-focused mindset doesn’t erase difficulties, but it does give you the resilience to push through them.

With the right perspective, you can:

- 💪 See your worth beyond your bank balance

- 🔄 Turn setbacks into comebacks

- 🎯 Get creative about solving money problems

- 🔥 Use failure as fuel for growth

- 🚀 Pair hope with consistent action to unlock your potential

My Journey: Humble but Hopeful Beginnings 🌱

Like many, I started with financial struggles. I had big dreams to become a millionaire by age 30—but without a plan, that dream quickly faded. What I held onto, though, was a mindset of determination.

Even when I was broke, dealing with unexpected car repairs, or scraping by paycheck to paycheck, I refused to let those moments define me. I knew being “poor” wasn’t my identity—it was a temporary state.

Over time, I realized:

- Success isn’t about wealth alone.

- Every struggle can become a stepping stone.

- Believing in your ability to grow is the first step toward real change.

Breaking the Poverty Mindset: Why Hope Matters 💭

Too many people today lose hope when life gets hard. They confuse “being broke” with “being poor.”

Here’s the difference:

- Being broke 💵 is temporary—it’s a financial situation.

- Being poor 🚫 is a mindset—a belief that things will never improve.

When you adopt a poor mindset, motivation disappears. But if you choose to see obstacles as opportunities, you give yourself the power to change your personal finances.

5 Practical Steps to Build a Growth-Oriented Financial Mindset 🔥

A mindset shift is powerful, but it needs to be backed by action. Here are five practical steps to get started:

1. Improve Your Money Knowledge 📚

Education is the ultimate wealth builder. Start small—read books, listen to podcasts, or take online courses. Over time, your confidence and financial literacy will grow.

Books that changed my money mindset:

- The Millionaire Next Door by Thomas Stanley

- Set for Life by Scott Trench

- Total Money Makeover by Dave Ramsey

Podcasts worth your time:

2. Track Your Spending & Create a Budget That Works 📝

You may be surprised how much slips away on restaurants, subscriptions, or small impulse buys. Track every dollar for a month—you’ll see patterns clearly and improve your budgeting.

From there, create a budget that lets you spend on what you love and cut back on what doesn’t matter as much.

📊 Take control of your finances today: Learn how to create a budget that really works!

3. Set Financial Goals and Plan Your Ideal Lifestyle 🌟

Think about the lifestyle you want and write it down. Break it into smaller, achievable milestones, and use them to build momentum toward your vision.

4. Rethink Your Relationship With Money 💡

If you see money as the root of all evil, you may unconsciously hold yourself back. Instead, view money as a tool that creates freedom and expands your options.

5. Practice Generosity 🎁

Giving reinforces an abundance mindset. Even small acts of kindness or intentional giving show that money is a resource to be shared, not hoarded.

The Bottom Line ✅

Believing “poor is a state of mind” doesn’t mean mindset is the only factor in financial success—but it is a foundational one. When you pair a positive outlook with education, discipline, and consistent action, you give yourself the best chance to break free from limitations, overcome adversity, and build the future you want.

You already have the power to shift your mindset. Now it’s time to use it. 💡